Insurance

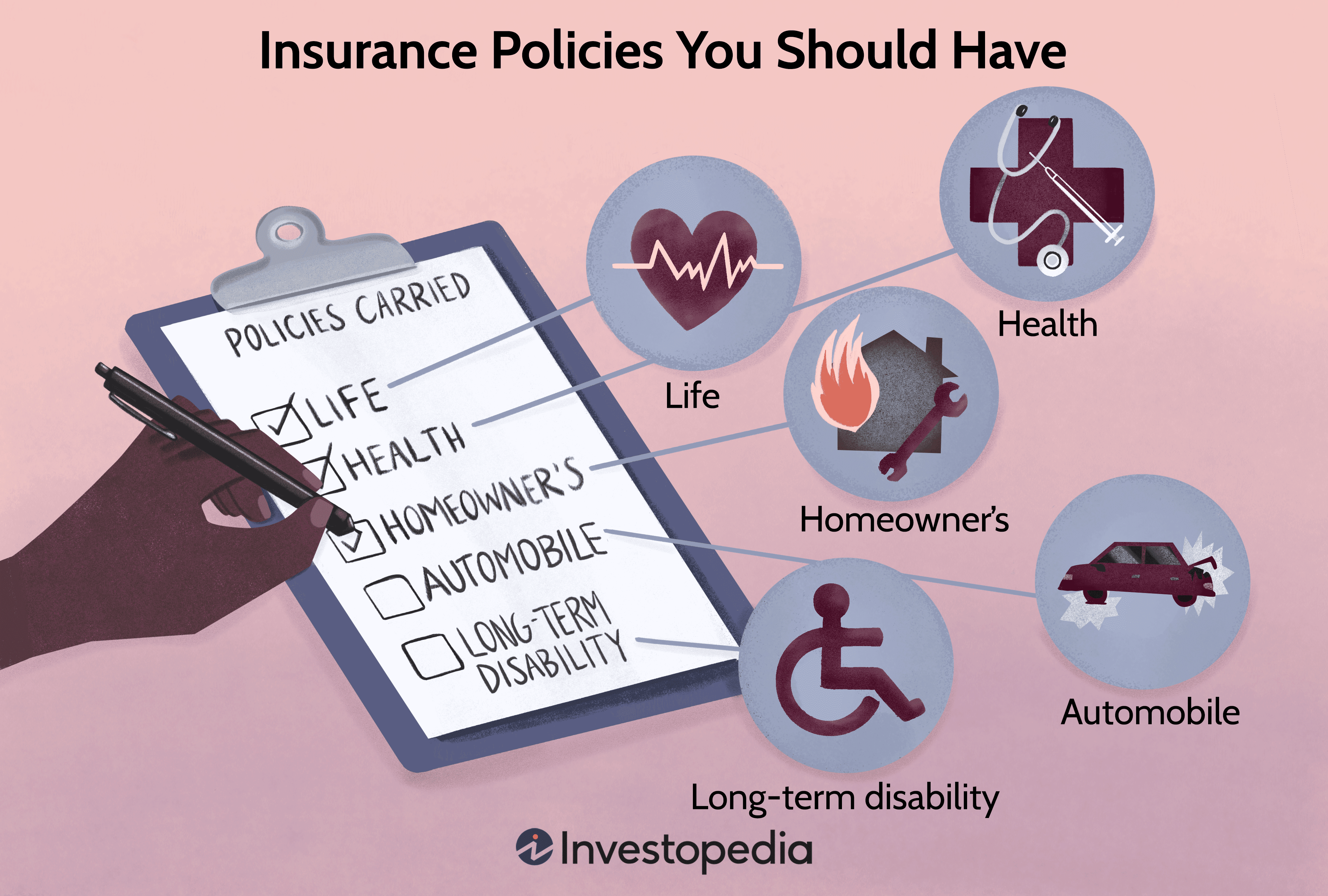

Insurance is a broad topic that includes protections of homes, cars or boats, personal health, and life itself. It is designed to protect against financial loss resulting from unforeseen circumstances by sharing or pooling the risk of loss with other policyholders.

Insurance Basics

-

How do insurance companies make money?

Insurance companies generate revenue from premiums paid on outstanding policies and net profit on the difference between revenue and policy claim expenses.

-

How does an insurance broker make money?

Insurance brokers typically earn commissions on the sale of policies, either on a flat rate per policy or on a percentage of the insured amount.

Learn More: How Does an Insurance Broker Make Money? -

Why do insurance policies have deductibles?

Insurance policies often have deductibles, especially with health and auto insurance, in order to partially offset the cost of providing coverage by the company and can keep premiums lower if customers opt for higher deductible amounts.

Learn More: Why Do Insurance Policies Have Deductibles? -

Do men and women pay the same for insurance coverage?

There is definite gender bias in insurance coverage depending on type of insurance. With auto insurance there can be gender discrimination tied to income and credit scores, while with life insurance women generally pay lower rates due to longer life expectancy.

Learn More: Gender and Insurance Costs -

Can bundling insurance policies save money?

Yes, insurance carriers typically offer significant discounts for those who have multiple types of coverage with their company, such as bundling car and homeowners insurance.

Learn More: Bundle Your Insurance for Big Savings

-

Insurance Coverage

Insurance coverage refers to the amount of protection within an insurance policy that covers a specific type of loss. Coverage is typically meant to completely replace the value of the insured item or items. In the case of life insurance the coverage amount is typically based on a fixed amount or calculated on a multiple of years of lost income should the insured person die.

-

Insurance Premium

An insurance premium is the amount of money the customer pays to the insurance underwriter each month to maintain the policy. Insurance premiums cover the cost of providing coverage by the insurance company based on the risk or probability of loss.

-

Insurance Underwriter

An insurance underwriter is the company that takes on the risk of covering a specific type of loss event in exchange for payment of premiums during the term of the policy. Insurance underwriters pool the risk of loss across large numbers of policyholders and set premiums based on the managed risk of coverage.

-

Insurance Claim

An insurance claim is the notification of the underwriter by the policyholder that a covered loss has occurred. Insurance companies have specific processes for policyholders to file insurance claims in the event of loss along with service level expectations for claim processing that are detailed in the insurance policy contract.

-

Insurance Adjuster

An insurance adjuster is an employee of the insurance underwriter who investigates covered loss claims and authorizes payouts. Once the policyholder files a claim and insurance adjuster will contact the policyholder to understand the time, date and nature of the covered claim and make an adjustment or payment based on eligibility, less any deductible.

-

Self Insurance

Self insurance is a process by which a person or company assumes the risk of loss themselves by saving the money that would have otherwise been paid in the form of premiums in order to build up a fund to cover potential losses. Individuals that choose to self insure bare all the risk for a loss event rather than pooling the risk with other people who might also experience the type of loss that might present financial loss.

Explore Insurance

:max_bytes(150000):strip_icc()/unemployment_480991253-6ca6d91677ee49dcbb3e942242fcb8e5.jpg)

:max_bytes(150000):strip_icc()/elizabethtaylorprivatefuneral-56a34e0b3df78cf7727cceff.jpg)

:max_bytes(150000):strip_icc()/dv740090-5bfc2b8b46e0fb00265bea71.jpg)

:max_bytes(150000):strip_icc()/reinsurance.asp-final-da298221a9b342d58efb513d1eb48803.png)

:max_bytes(150000):strip_icc()/underwriter-FINAL-3332984c296246d288116b477d647eca.jpg)

:max_bytes(150000):strip_icc()/underwriting-4187414-1-faf1d6b3110546b6a4e351c51f6db84b.jpg)

:max_bytes(150000):strip_icc()/indemnity.asp-final-a0e5f0844e884e3ab1d76354f00e3f8b.png)

:max_bytes(150000):strip_icc()/insurance_claim.asp-final-ad2bc2c60d5c46e999bf064a90ff2dc6.png)

:max_bytes(150000):strip_icc()/umbrella-2904775_1920-d61c2ad2409a446aab33a7c0a9080607.jpg)

:max_bytes(150000):strip_icc()/GettyImages-1141164585-5486d44770c94a2784185a75be37a6fa.jpg)

:max_bytes(150000):strip_icc()/insurance-underwriter.asp-final-0e106b06a1c2405d9add3a36946690fd.png)

:max_bytes(150000):strip_icc()/hand-putting-wooden-five-star-shape-on-table--the-best-excellent-business-services-rating-customer-experience-concept-1029077200-9691eb3167d24c8bbcd09e8a839a38ec.jpg)

:max_bytes(150000):strip_icc()/high-school-students-5bfc2b8b46e0fb0083c07b7d.jpg)

:max_bytes(150000):strip_icc()/waiver-of-subrogation.asp-final-fff580d968404949b7347471c2795978.jpg)

:max_bytes(150000):strip_icc()/combinedratio.asp-final-90d3b1a5d0cf455eb998651d813d71e5.png)

:max_bytes(150000):strip_icc()/GettyImages-1125625723-37ef6b9d36e64067a6609f35bac1d1b5.jpg)

:max_bytes(150000):strip_icc()/GettyImages-184985261-257061c6b35546779a16b51ca1e9da8e.jpg)

:max_bytes(150000):strip_icc()/GettyImages-1141794014-43b2241017694328a0a104a92ca37193.jpg)

:max_bytes(150000):strip_icc()/thinkstockphotos_80410231-5bfc2b97c9e77c0026b4fb20.jpg)

:max_bytes(150000):strip_icc()/GettyImages-944975896-1e117f457b9f4b72a623b9befa6a3c3e.jpg)

:max_bytes(150000):strip_icc()/GettyImages-1181008199-180a5cf02e8640d088691d57f1c5efb3.jpg)

:max_bytes(150000):strip_icc()/GettyImages-1053743626-21039c92e4b44b828f71db2c1d27a9a2.jpg)

:max_bytes(150000):strip_icc()/shutterstock_253136563-5bfc2b98c9e77c00519aa7a8.jpg)

:max_bytes(150000):strip_icc()/200275051-001-5bfc2b8b46e0fb0083c07b92.jpg)

:max_bytes(150000):strip_icc()/young-couple-with-receipts-and-documents-using-calculator-200441351-001-5774302f5f9b585875824b32.jpg)

:max_bytes(150000):strip_icc()/Takaful_final-b92564eedb654588b36c9c7c2b3e5031.png)

:max_bytes(150000):strip_icc()/GettyImages-1175219554-d2d59c24adcb41cd960f497ac3df098b.jpg)

:max_bytes(150000):strip_icc()/business_building_153697270-5bfc2b9846e0fb0083c07d69.jpg)

:max_bytes(150000):strip_icc()/thinkstockphotos_493208894-5bfc2b9746e0fb0051bde2b8.jpg)

:max_bytes(150000):strip_icc()/health_insurance_464403251-5bfc375846e0fb00260e24bc.jpg)

:max_bytes(150000):strip_icc()/shutterstock_313802690-5bfc2b5446e0fb0051bdd5d0.jpg)

:max_bytes(150000):strip_icc()/thinkstockphotos-477852728-5bfc34d646e0fb00511b6830.jpg)

:max_bytes(150000):strip_icc()/4-types-of-insurance-everyone-needs.aspx-final-f954e12eb3074b178e4b53a882729526.jpg)

:max_bytes(150000):strip_icc()/GettyImages-946934494-6217dbb20474437bb6c780630f99393e.jpg)

:max_bytes(150000):strip_icc()/financial-advisor-having-a-meeting-with-clients-1063753064-d30910ffcb3e4ccc8133832222874929.jpg)

:max_bytes(150000):strip_icc()/calculating-premium.asp_sketch_revised-a342201375164378925271cdad1f1929.png)

:max_bytes(150000):strip_icc()/122582497-5bfc2b8d46e0fb005119b24b.jpg)

:max_bytes(150000):strip_icc()/what-main-business-model-insurance-companies.asp-FINAL-092abcf238d348c4975e1021489191e6.png)

:max_bytes(150000):strip_icc()/ServiceDog-75e1e8cc5897438b805ca018da5b8f55.jpg)

:max_bytes(150000):strip_icc()/construction2-2764b203c52d49feaf16e6cf7a68bd70.jpg)

:max_bytes(150000):strip_icc()/womanwithdog-0f75bd9dd01a4576a7eec879b5e804ba.jpg)

:max_bytes(150000):strip_icc()/shutterstock_112522391-5bfc2b9846e0fb0051bde2d3.jpg)

:max_bytes(150000):strip_icc()/DuPont-Return-on-Equity-Analysis-ROE-56a091b63df78cafdaa2cf2d.jpg)

:max_bytes(150000):strip_icc()/147323400-5bfc2b8c4cedfd0026c11901.jpg)